Key Takeaway: Michael Saylor introduced a simple but powerful framework to determine whether companies holding Bitcoin can outperform BTC itself—and it all comes down to the cost of debt versus Bitcoin’s returns.

The Two Numbers You Need to Know

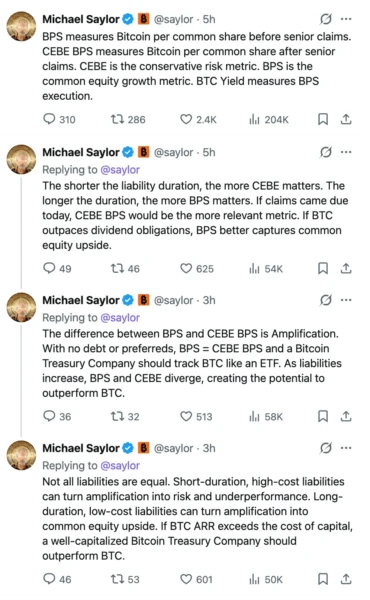

Michael Saylor, Executive Chairman of MicroStrategy (MSTR), just laid out a clear framework for evaluating Bitcoin treasury companies. And it starts with two metrics that might seem simple but tell you everything:

BPS (Bitcoin Per Share)

This measures how much Bitcoin backs each common share before accounting for debt or preferred shares. Think of it as the happy scenario—what each share would be worth if the company had zero liabilities.

If a company is essentially a pure Bitcoin holder with no debt, BPS is your whole story. It’s basically a Bitcoin ETF wrapped in a corporate shell.

CEBE BPS (Common Equity Bitcoin per share)

Here’s where it gets real. CEBE measures Bitcoin per common share after the company pays off everything it owes—debts, preferred shares, you name it.

Saylor’s way of framing it: BPS shows the upside, CEBE shows the floor. One’s optimistic, one’s conservative.

The Secret Ingredient: Amplification

Here’s the insight that matters: the gap between BPS and CEBE BPS is what Saylor calls “Amplification,” and this gap is everything.

No debt? No amplification. The stock should move roughly in line with Bitcoin, like an ETF would.

Carrying debt or preferred shares? Now you’ve got amplification, and it can cut both ways.

When Leverage Works For You

Imagine a company borrows cheaply and locks in that rate for years. With that borrowed cash, they buy more Bitcoin upfront. As Bitcoin rises, that extra Bitcoin creates bigger gains for shareholders than they’d get if the company carried no debt at all.

That’s the leverage working in your favor.

When Leverage Works Against You

But—and this is the crucial “but”—not all debt is equal.

If a company takes on expensive debt with a short repayment timeline, the tables turn fast. That leverage becomes a weight around the neck. The company might be forced to sell Bitcoin or issue new shares just to make payments, regardless of where Bitcoin’s price sits. That’s no longer amplification. That’s a drag on returns.

Saylor’s One-Line Test (That Actually Matters)

Forget the complexity. Saylor boils it all down to a single benchmark:

If Bitcoin’s annualized return exceeds the company’s cost of capital, a well-capitalized Bitcoin treasury company should outperform Bitcoin.

That’s it.

If Bitcoin’s yearly gains are bigger than what it costs the company to borrow, the debt helps shareholders. If Bitcoin’s gains don’t cover the cost of borrowing, that same debt becomes a burden—even if the company holds more Bitcoin than before.

What This Means For MicroStrategy’s Stretch (STRC)

Saylor’s framework isn’t academic—it’s built with his own company in mind.

MicroStrategy’s preferred stock product, Stretch (STRC), pays holders a high dividend yield. Under Saylor’s model, STRC is textbook amplification. Whether it helps or hurts common shareholders depends entirely on whether Bitcoin’s returns beat the cost of those preferred shares.

It’s not a judgment call. It’s math.

The Bottom Line

Michael Saylor has given investors a framework to stop guessing and start calculating. A Bitcoin treasury company can beat Bitcoin—but only if the math works. Long-duration, low-cost debt? That’s your friend. Short-duration, expensive liabilities? That’s your enemy.

The stock market doesn’t always reward understanding, but at least now you know what to look for.

Meta: This article explains Michael Saylor’s framework for evaluating Bitcoin treasury companies, helping readers understand when leverage amplifies returns and when it becomes a drag on performance.

Leave a comment